Is This A Defining Moment For The Bond Market?

Kameleon007/iStock by using Getty Pictures

By Kevin Flanagan

It appears to be every single calendar year we examine commentary expressing that the “great bond current market bull run” is coming to an finish. And you know what? It has but to materialize. With U.S. bond market yields growing to concentrations not found given that 2018–19, industry individuals seem to be debating irrespective of whether premiums have even further place to increase from in this article or whether or not the will increase now depict a renewed acquiring possibility to go extensive length. As a result the title of this weblog article: Is This a Defining Second for the Bond Industry?

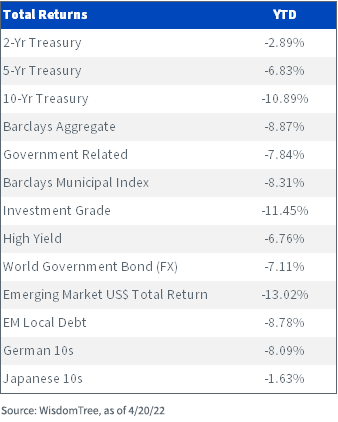

Ok, you might be inquiring: am I becoming a small overdramatic listed here? Effectively, let’s take a glimpse at the chart under to see wherever I’m coming from. As of this producing, there have been very little but detrimental readings in just about each individual major location or sector of the broader world wide set revenue arena. It’s not like we haven’t noticed crimson ink in the bond current market in the past, but the magnitude of the negative returns calendar year-to-day is very staggering in some scenarios.

I’m a big proponent of not chasing yesterday’s trade, which is why we have to have to question ourselves, exactly where do we believe the bond current market is headed from here? Let us use the U.S. Treasury (UST) market as our benchmark for the discussion. The rise in (UST) yields as a result much in 2022 has been due to Fed price hike anticipations as properly as the prospects for quantitative tightening (QT). A case can be made that UST yields have now factored in the hawkish pivot by the Fed, but I would argue that premiums have not concluded their ascent to greater floor yet.

To start with of all, the Fed has only lifted fees when this year and has not even started to employ QT. The pairing of these two tightening procedures as outlined by Powell & Co. up to this position can be a powerful power, and arguably, has under no circumstances been tried prior to. In addition, the recent pricing for Fed Cash Futures just gets us back again to neutral, whereby persistent inflation would possibly power the Fed to get monetary coverage into restrictive territory.

What about support from the worldwide trader? Really do not search now, but non-U.S. sovereign debt yields have been rising as effectively. In actuality, try to remember all individuals tales about common damaging world-wide bond yields? Let us just say that is now record. Applying the German 10-yr bund as our proxy, the produce amount has risen more than 100 foundation details (bps) yr-to-date, and the absolute level is just less than the 1% threshold. As not too long ago as December, the bond produce was all-around -.40%.

Probably, the most noteworthy factor is authentic yields, a.k.a. Ideas yields. In my impression, the the latest surge in the UST 10-Yr generate has been the immediate consequence of the maximize in true yields. Given that March 8, the 10-Yr Tips produce has skyrocketed by additional than 100 bps, and what was at the time a rate of -1.08% basically got down to zero previous week. Throughout the previous level hike cycle in 2018, the 10-Year Recommendations yield attained a superior watermark of 1.16%, or near to 120 bps over the place it resides as I compose.

Conclusion

Now, I’m not predicting that UST yields will raise by one more 100 bps. Nevertheless, the things I outlined in this site submit would feel to point to the probable for a bond current market generate like the UST 10-12 months to not only revisit its new peak of 3.25%, but also overshoot that reading through to the upside.

Kevin Flanagan, Head of Fixed Income Technique

As section of WisdomTree’s Financial investment Tactic group, Kevin serves as Head of Mounted Profits Strategy. In this function, he contributes to the asset allocation staff, writes fastened money-associated information and travels with the sales team, conducting consumer-experiencing meetings and offering skills on WisdomTree’s present and potential bond ETFs. In addition, Kevin functions carefully with the fixed money staff. Prior to signing up for WisdomTree, Kevin put in 30 decades at Morgan Stanley, wherever he was most not long ago a Handling Director. He was liable for tactical and strategic suggestions and produced asset allocation versions for fixed cash flow securities. He was a contributor to the Morgan Stanley Wealth Management World wide Investment decision Committee, principal creator of Morgan Stanley Wealth Management’s regular monthly and weekly fastened revenue publications, and collaborated with the firm’s Investigate and Consulting Group Divisions to make ETF and fund supervisor asset allocation versions. Kevin has an MBA from Tempo University’s Lubin Graduate University of Small business, and a B.S in Finance from Fairfield University.

Editor’s Note: The summary bullets for this report had been selected by Trying to find Alpha editors.