Taking Profits In Kraft Heinz (NASDAQ:KHC)

da-kuk/E+ via Getty Images

Since I put out my cautious piece on Kraft Heinz Company (NASDAQ:KHC) a couple of months ago, the shares have returned about 17% against a loss of about 10.7% for the S&P 500. I don’t feel too bad about this call, though, as I continue to hold shares and the puts I sold have lost the vast majority of their value. In this piece, I want to try to work out whether or not I should add to my position. I’ll make that determination by looking at the most recent financial performance, and by looking at the stock as a thing distinct from the underlying business. I’ll also compare this stock to the 10-year treasury note, because I’m of the view that the “TINA” argument is reversing. We stock investors should be aware of the fact that a rise in the risk free rate raises the rate at which we discount future cash flows, which affects prices of all assets today.

In case you missed the title of this article, and in case you fired past the three bullet points above, I’ll share my thoughts in this, the so-called “thesis statement” paragraph. I think Kraft Heinz is a fine business, and the most recent financial performance was great. The problem is that the shares aren’t objectively cheap. This is even more troubling when you compare the cash flows a stock investor might receive with the cash flows a treasury note investor is certain that they will receive. In a world where the risk free rate is over 3%, a stock has to be very compelling to “make the cut”, and unfortunately at current prices Kraft Heinz isn’t that compelling in my view. For this reason, I’ll be selling my shares. At the same time, the puts I sold for $0.39 previously are currently bid at $0.01. Since I’d be very comfortable buying the stock at $27.50, I’m taking no action on these.

Financial Snapshot

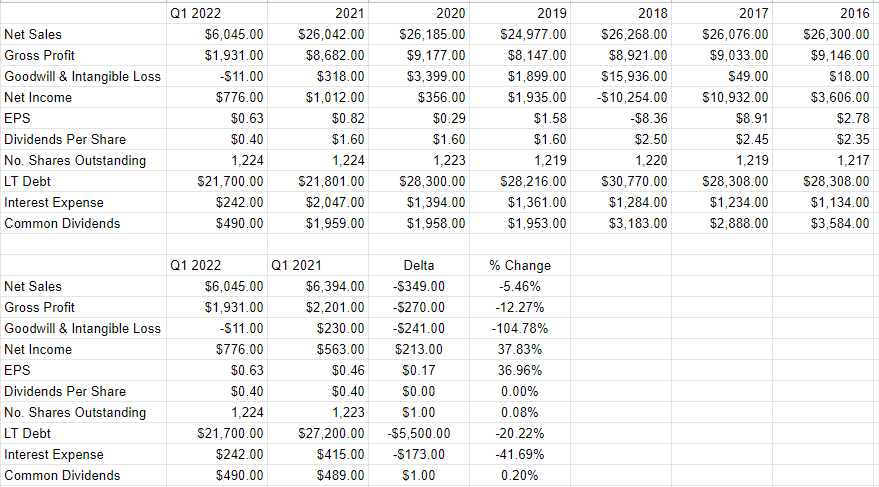

I’d say that the most recent quarter produced results that were mostly positive. For instance, while revenue was down about 5.5%, net income was up by just under 38%. This was driven by a $79 million (1.9%) reduction in COGS, a $55 million (6.24%) reduction in SG&A, and the fact that goodwill impairment losses swung from $230 million this time last year, to a reduction of $11 million this year. Finally, it didn’t hurt that interest expenses dropped $173 million or 41.7% relative to the prior period. Most importantly, I really like the fact that long term debt cratered relative to 2021, down fully $5.5 billion.

I’ve written in earlier notes on this name that I think that the dividend is reasonably well covered. If you’re interested in my thinking on that front, I’d encourage you to revisit those earlier articles, as I don’t want to go over previously trodden ground now. Suffice to say I think the financial results are reasonably good, and I’d be happy to buy even more shares at the right price.

Kraft Heinz financials (Kraft Heinz investor relations)

The Stock

I’ve made the point that a stock is quite distinct from the underlying business to the point of tedium. The business buys a number of inputs, including labour, performs value adding activities to those, and sells the results at a profit. In the final analysis, that’s what every business is. The stock, on the other hand, is a traded instrument that reflects the crowd’s aggregate belief about the long term prospects for a given company. The crowd changes its views very frequently which is what drives the share price up and down. It’s typically the case that the lower the price paid for a given stock, the greater the investor’s future returns. In order to buy at these cheap prices, you need to buy when the crowd is feeling particularly down in the dumps about a given name. This is easier said than done.

I measure the relative cheapness of a stock in a few ways ranging from the simple to the more complex. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. Once again, cheaper wins.

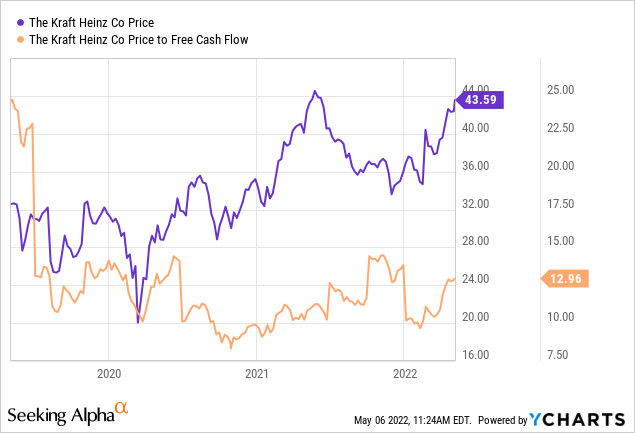

In the previous article on this name, I became aggressively bullish when the price to free cash flow hit ~12.10 times, and refused to add to my position when the valuation hit a price to free cash of ~14.7. Once again, shares are relatively cheaper on that measure, per the following:

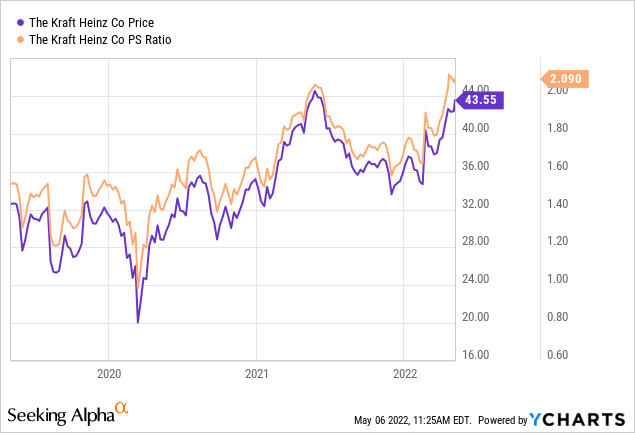

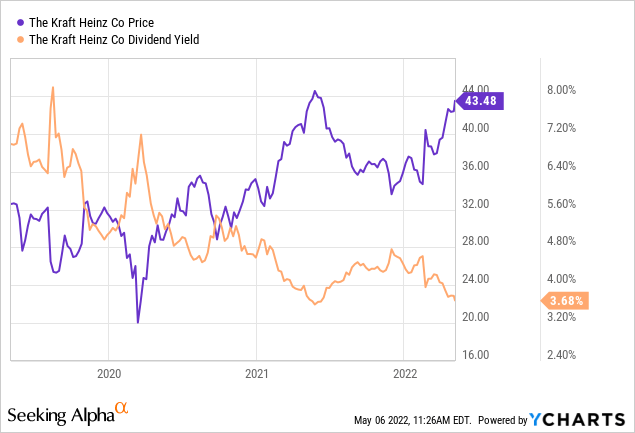

I should point out that in some ways the shares are actually rather expensive. On a price to sales basis, for instance, they’re trading at or very near multi year highs, per the following:

At the same time that investors are paying near multi-year high levels for $1 of future sales, investors are receiving near recor

d low yields, per the following:

I’m not a fan of paying more and receiving less.

In addition to simple ratios, I want to try to understand what the market is currently “assuming” about the future of this company. In order to do this, I turn to the work of Professor Stephen Penman and his book “Accounting for Value.” I’ve heard from some people in my so-called “real world” that this book is a bit too academic, and so you may want to check out “Expectations Investing” by Mauboussin and Rappaport, which is a book that goes over the same ideas in a slightly more accessible way. Anyway, the idea is to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in the said formula. Applying this approach to Kraft Heinz at the moment suggests the market is assuming that this company will grow at a rate of about 12% over the long term. This is a massively optimistic forecast in my view. For that reason, I’m inclined to avoid the stock at the current price.

But Wait, There’s More…

In the domain of investing, everything is relative. If we buy a stock, by definition we’re eschewing countless other stocks. This dynamic applies to different asset classes, too. If you buy stocks, you’re not buying gold bars or beanie babies, or fine art or farm land. I think it’s helpful to sometimes review the relative merits of our favourite asset classes and to check our assumptions to see if they are still valid.

For instance, for years I’ve heard the argument that investors must buy stocks because the returns from government bonds are paltry. When the 10-year Treasury note was yielding 1.3% nine months ago, why would you lock in for such a pittance? That was a fair argument that made some sense. Now that the 10-year note has climbed above 3%, I think we would be wise to take a minute to review the relative merits of stocks versus bonds.

In the following analysis, I’m going to compare the cash flows from the stock dividend to the cash flows from the treasury note. While this analysis won’t answer whether it’s preferable to buy this stock or a 10-year note, I think it’ll go some way toward defining for us what growth we need from the stock to be indifferent between owning that stock or treasury. I should say that I don’t perform analyses like these to try to forecast a “to the penny” comparison between these two alternatives. I want to get a sense for the cash flow “margin of safety” for the stock relative to the bond. In other words, if the stock investor barely receives more cash than the owner of the 10-year treasury, that’s a bad sign. The reason for this is the former is fraught with unpredictability, while the latter, for its many faults, is not.

After dropping 36% in 2019, the Kraft Heinz dividend has remained constant since. Thus, I’m comfortable assuming the future dividend growth rate will be very close to zero. That said, I also want to forecast the dividend growing at the approximate rate of the economy (~2%). Again, I’m not trying to work out a precise estimate. I want to see how close or far the future dividend cash flows of this company will be from the guaranteed interest payments on a 10-year Treasury.

Assuming zero growth, the stock investor will receive ~$1,300 more in dividend income than the treasury owner. Assuming the dividend grows at a CAGR of 2%, the stock owner receives an extra $1,940 of income over the next decade.

A Comparison of Dividend v Treasury cash flows over the next 10 years (Author calculations from public sources)

In my view, the investor has to ask themselves whether or not they’re comfortable taking on the various risks associated with this stock for an extra $130-$194 in income for each of the next 10 years. For my part, I prefer to sleep at night, so I won’t.

Conclusion

Although the shares are pretty expensive on a price to sales basis, and the dividend is near record low yields, in a different world I might consider nibbling on this stock again. In a world of a 3% risk free rate, though, I won’t. The relative risk is too great, and the relative rewards from stock ownership are too puny in my view. For that reason, I’ll be taking profits in my Kraft Heinz stock. Also, in my previous missive, I recommended selling the July Kraft Heinz puts with a strike of $27.50 for $0.39 each. They’re currently bid at $0.01, and I’d be happy to buy the stock for $27.50, so I’ll take no action on those. In my view, stocks in general are becoming less attractive, and we should start thinking about how the inversion of the TINA idea will affect their prices.